Asset Allocation: A perfect key to help you achieve your future financial goals.

You might have seen many financial advisors and asset management companies that put through creative advertisements in order to emphasize the need of asset allocation in investments. Have you ever wondered why this concept is so important for the individual investors like you and me to comprehend? Let us take a quick look at it.

Imagine yourself to be an owner of a small startup, if you want to grow your business what type of talent would you attract? Hire the best talent with different abilities and skill sets to make a good mix of these people in a team. In order to grow your business multifold, it is important to have a good mix of people with different thinking perspectives, skill sets and creative outlooks. Similarly, in your portfolio you need all kinds of asset classes ranging from Bonds, equities, gold, commodities and real estate which may perform in different market conditions. A good team mix can be a mantra for growing your startup and asset allocation can be a mantra for a winning portfolio.

What is Asset Allocation?

Asset allocation is the process of deciding how to divide your investment across several asset categories. Stocks, bonds, Mutual funds, other debt instruments, and cash or cash alternatives are the most common components of an asset allocation strategy. Asset allocation means diversifying your portfolio. The construction of the portfolio involves allocating money to various asset classes. This process is called Asset Allocation.

The most famous phrase you might have heard is ‘Never put all your eggs in one basket’.This phrase perfectly describes asset allocation and underlines the importance of diversification in mutual funds. Where prudency lies in choosing those schemes which offer sectoral diversification to minimize the market risk or systematic risk in mutual fund investments to help you gain higher returns. As all asset classes don't move at the same pace or in the same direction and that's why having the right mix is important.

In simple words invest your money in different types of an investment product to minimize your risk and maximize the returns. The asset class can be cash, equity, debt, real estate and gold. Asset Allocation depends upon your age, risk-taking ability and time horizon for the particular goal. Asset Allocation also provides for a direction to the future income and cash flows of the investor in terms of where he should invest to achieve his/her financial goal.

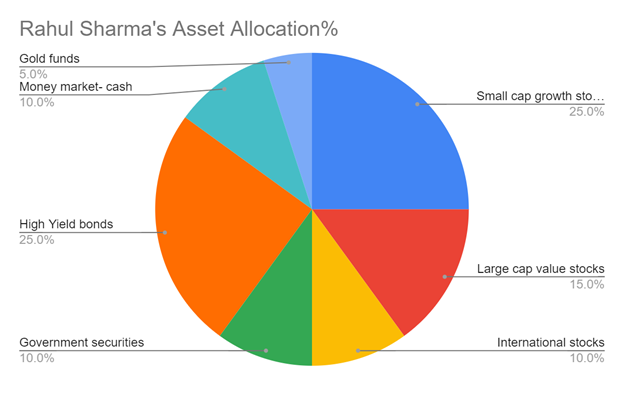

Let’s take an example to practically understand Asset Allocation: Rahul Sharma is in the process of creating a financial plan for his retirement. Therefore, he wants to invest his Rs 10,00,000 savings for a time horizon of five years. So, his financial advisor may advise Rahul to diversify his portfolio across the three major categories at a mix of 50/40/10 among stocks, bonds, and cash. The asset allocation may look like:

| Asset class | Category | Allocation% |

|---|---|---|

| Stocks | Small cap growth stocks | 25% |

| Large cap value stocks | 15% | |

| International stocks | 10% | |

| Bonds | Government securities | 10% |

| High Yield bonds | 25% | |

| Cash | Money market-cash | 10% |

| Gold | Gold funds | 5% |

*source: Author’s calculations.

The analysis suggests that, the distribution of Rahul’s investment is across three broad asset classes namely Stocks, Bonds and Cash equivalents. Such distribution reduces the level of volatility associated with the portfolio. The asset allocation here is made on the basis of the financial goals and risk tolerance of the investor. Since Rahul wanted to plan his retirement fund and fund portfolios, he should be able to balance between two conflicting needs: preservation of capital for safety, and growth of capital to protect against inflation. This balance can be possible when the allocation has distributions in both stocks and bonds and a percent of it in cash equivalents.

What is the importance of Asset Allocation?

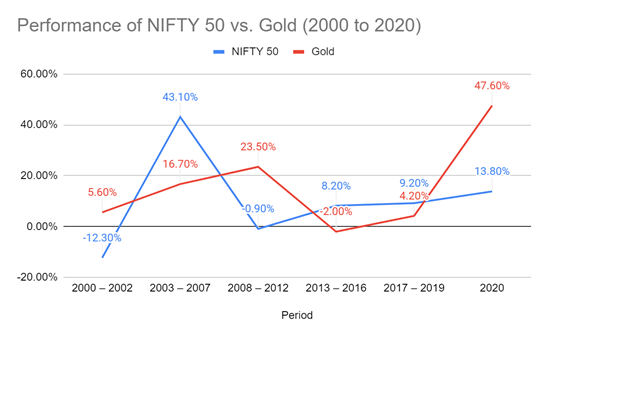

Different asset classes move in different directions. All types of asset classes hardly perform in tandem with each other. One might assume that it is best to invest in those Mutual funds that are performing really well at a particular time with an aim to time the market. However, it is quite challenging for any individual to predict in which direction any asset class would move at any given point of time. For instance, when equities may go up, gold investment might go down and vice versa. So, it makes sense to allocate investments in a mix of asset classes. This is done so that if one set of asset classes or funds underperforms, the other asset classes will balance the underperformance. Investing one’s portfolio in just one asset class or mutual fund scheme can be extremely risky. However, if an investor’s wealth is spread across asset classes, they tend to make better returns as diversification refers to investing into those asset classes that are not correlated in terms of performance. To understand this better, consider the following table that shows the performance of the NIFTY 50 Index (which represents the performance of equities) vs. Gold for the 2000 to 2020 period.

Performance of NIFTY 50 vs. Gold (2000 to 2020)

| Period | NIFTY 50 | Gold |

|---|---|---|

| 2000 – 2002 | -12.30% | 5.60% |

| 2003 – 2007 | 43.10% | 16.70% |

| 2008 – 2012 | -0.90% | 23.50% |

| 2013 – 2016 | 8.20% | -2.00% |

| 2017 – 2019 | 9.20% | 4.20% |

| 2020 | 13.80% | 47.60% |

* Source: Bloomberg

In the table above, you can see that the performance of equities and Gold have shown weak correlation over an extended period,i.e., when NIFTY 50 has outperformed, Gold has underperformed. This is the key reason why these two can be considered as diversified asset classes suitable for developing a good asset allocation strategy. Now that you know the different types of assets that you can invest in, let us discuss a few of the commonly used asset allocation strategies.

Types of Asset Allocation Strategies

Asset allocation strategies are classified into 2 major categories – Strategic Asset Allocation and Tactical Asset Allocation.

- Tactical Asset Allocation: It consists of techniques that aim to improve risk-adjusted portfolio returns by taking advantage of short-term opportunities while simultaneously staying on course to achieve long-term investment objectives.

- Strategic Asset Allocation:Investors may use different asset allocations in order to fulfill diverse financial objectives. Someone who is looking forward to purchasing a car next year, for example, might invest their car savings fund in a very conservative mix of cash, certificate of deposits(CD’s) and short duration bonds. An individual who is saving for retirement that may be decades away typically invests the majority of his savings in stocks, since he may have a lot of time to ride out the market's short-term fluctuations. Risk tolerance plays a key factor as well. Someone who is uncomfortable investing in stocks may put their money in a more conservative allocation irrespective of the long duration investment horizon and lock in period.

This type of allocation is done with a goal to generate maximum returns while keeping the risks in control which is acceptable to the investor. Now, Strategic Asset Allocation is one of the important concepts in portfolio management theory.The two main principles are :

- Diversification of portfolio

- Reduced Risk with good returns.

These two objectives can be achieved through timely rebalancing of the portfolio, which is an important concept of strategic asset allocation. This is because timely rebalancing of the portfolio will help to reduce the risk exposure due to company specific, economic or political linkages which have an impact on the markets and in turn your returns. As the market is dynamic, rebalancing of the portfolio is the key to consistency in achieving the expected financial goals.

Lets understand this concept with an example:

Suppose a portfolio has been constructed with 60% debt and 40% equity in the beginning. But at the end of the year when the portfolio was reviewed, it was found out that equity now represents 50% of the portfolio as the equity market had performed well during the year. So how do we re-balance it to its original?

The equity portion will be sold to bring it to 40% and with that proceeds debt will be bought in order to bring it up to 60%, as shown in the table below:

| Asset allocation | Target allocation | Current allocation | Adjustment | Final allocation |

|---|---|---|---|---|

| Equity | 40% | 50% | Sell off 10% equity | 40% |

| Debt | 60% | 50% | Buy debt to the extent to 60% | 60% |

Strategic Asset allocations are less automated as compared to a tactical asset allocation and you can customize it according to your financial goals and long term commitments. There are two different strategic asset allocation techniques : Age-Based Asset Allocation and Risk-Based Asset Allocation.

- Age- based Asset Allocation: In the age-based asset allocation technique, the investment decision is based on the age of the investor using the following formula: Percentage of Equity in Portfolio = (100 – Age of Investor). While this approach does provide a starting point for asset allocation, it is clearly not sufficient especially as it does not factor in key variables such as your investment objective or your risk tolerance. The second type of strategic allocation technique – risk profile-based asset allocation is designed to overcome this limitation.

- Risk Profile Based Asset Allocation This technique of strategic asset allocation is a significant improvement on the age-based method as it uses the investor’s risk tolerance in determining how investments need to be allocated across different types of assets. This method assigns investors the following 5 labels based on their ability to tolerate risk and volatility in their portfolio:

- Conservative

- Income

- Growth

- Aggressive

Conservative Income Growth Aggressive Domestic Equities 15% 25% 45% 55% International Equities 0% 0% 15% 20% Debt (Bonds) 80% 65% 20% 5% Gold 5% 10% 15% 20% Debt 60% 50% Buy debt to the extent to 60% 60% TOTAL 100% 100% 100% 100% *Source: Author’s research

So in the case of an aggressive investor, the risk-based asset allocation model recommends 75% equity allocation in total towards Domestic Equities and International Equities. Whereas in the case of a conservative investor, the total Equity allocation (including both domestic and international equities) is only 15%, while Debt instruments such as Bonds account for 80% of the portfolio. In the case of an income investor, the total Equity allocation (including both domestic and international equities) is 25%, while debt accounts for 65% of the portfolio.

Now let's look at the important factors that can affect your asset allocation for investments and how they help you arrive at the right mix of assets to achieve your goals?

The process of determining the right mix of assets for your portfolio is a very personal one. When making investment decisions, an investor’s asset allocation decision is influenced by various factors such as personal financial goals and objectives, risk appetite, and investment horizon. Let’s understand these factors.

- Time of horizon :- Time horizon is the number of months or years an investor is expecting to invest to achieve a particular goal. Different investment horizons entail different risk tolerance. For instance, a long-term investment horizon might prompt an investor to invest in a higher risk portfolio as the slow economic cycles and high volatilities in the market tend to ride out with time.

- Risk tolerance:- Risk tolerance refers to an investor’s willingness and ability to lose some or all of their original investment in anticipation of greater potential returns. Aggressive investors, or investors with a high risk profile are likely to risk most of their investments to get better returns. On the other hand, conservative investors, or risk-averse investors are likely to invest in securities that preserve their original investments.

- Risk vs returns :-Risk and returns are directly related but risk is a double edged sword. If you take too little risk, you may not be able to make the money needed for your financial goals. On the other hand, if you take too much risk, you will expose your financial goals to uncertainties of capital markets. Right asset allocation means that you take the optimal amount of risk to meet your short term, medium term or long term financial goals.

In closing

With asset allocation, the concept of ‘one size fits all’ does not apply. Every individual’s financial condition is different and requires a unique and different approach. In fact, an investor should regularly check their financial strategies and ensure that it aligns with their financial goals, risk profile and investment horizon. Remember, portfolios that have superior product selection and consistent asset allocation tend to outperform the market even in volatile markets. Investing all your money purely in one asset class can be disastrous, as the risk of losing all your money if the markets move south remains high. To beat this risk off, it's important to diligently practice asset allocation and rebalancing of your portfolio seeing the market conditions, whenever deemed necessary. The following are some key tips and strategies to help you plan your asset allocation strategy better:

- Don’t box yourself in : Instead of deciding ahead of time what kind of investor you are and acting accordingly, you should instead adapt to changing market conditions. This will allow you to use your asset allocation strategy to benefit from changing market conditions. If you box yourself in, you can end up missing out on big opportunities or end up taking significantly higher risks.

- Consider multiple factors to design your asset allocation strategy : When designing your asset allocation strategy, you need to consider various factors including your investment goals, current situation, risk appetite as well as investment horizon

- Have Multiple Strategies for Multiple Goals: It is a good idea to have different asset allocation strategies depending upon your specific goals. For example, the allocation strategy for your retirement goal which is 30 years away should not be the same as the goal of generating capital to start your own business 5 years down the line

- Weak Correlation between assets supports better asset allocation: Choosing asset classes that have low correlation is the key to creating a successful asset allocation plan.

- Periodically monitor and adjust allocation: It is necessary to periodically monitor and adjust your asset allocation over time through portfolio rebalancing to ensure that your portfolio performance matches your investment goals.